How does the French succession regime impact you and your family?

By Thomas Marron, Partner, Blevins Franks Beziers

Succession is one of the most misunderstood aspects of financial planning here in France. If you find it confusing, rest assured you are not alone. Here are a few misconceptions that we hear regularly: –

1. “French succession law doesn’t affect me – I have elected via my will for UK rules to apply instead”.

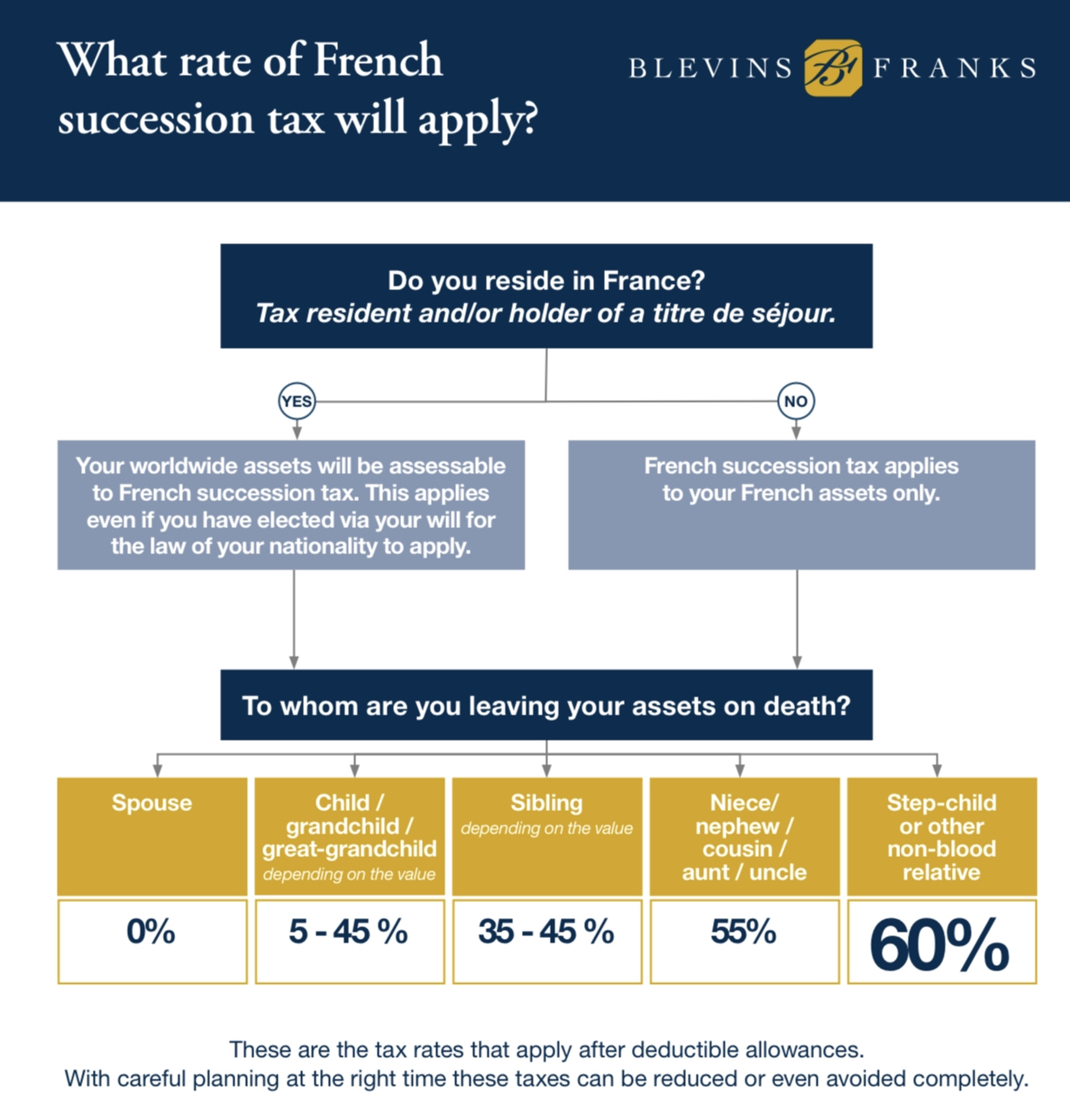

Since 2015 it has been popular for foreign nationals, including Britons, to utilise an EU law ‘Brussels IV’ that allows individuals to elect for the law of their nationality to apply to their estates instead of the more prescriptive French system. (The latter includes elements of forced heirship in favour of biological/adopted children – potentially disadvantageous to a surviving spouse). However, in 2021 France introduced a law that contradicts the EU legislation enabling protected heirs to ask for the application of French forced heirship rules, should assets pass under the provision of a country with no forced heirship rules. So until the domestic rule is successfully challenged in the European courts, for assets located in France, French succession law may apply to all residents of France upon their death even if they had made another choice of law under Brussels IV.

2. “I don’t need to worry about French succession tax. I have most of my assets in the UK”.

The situation here is simple: the worldwide assets of a French resident are assessable for French succession tax upon death, without exception. This includes UK property, bank accounts, shares, drawdown pension funds, and all other assets. French tax applies irrespective of the potential application of Brussels IV mentioned above. The rates of succession tax vary dramatically, depending on the relationship between the deceased and the beneficiary.

3. “I intend to gift all of my wealth away to my children / step-children / nieces and nephews / family friend, so that they avoid succession tax completely.”

This might seem a good strategy except for the existence of French gift tax, which applies at the same rates as succession tax, i.e. up to 60%. Gifting can be useful in a limited way, but the tax-free allowances are normally not enough to make a significant difference to large estates.

Planning options

If you find the above disheartening, it is worth considering that, with the right planning, the French system can be more advantageous than the UK one. There are numerous planning tools available that can allow you to ensure that monies pass into the right hands at the right time. A few examples are as follows:-

- There is a way of gifting assets while retaining a lifetime right of enjoyment. This is known as a ‘usufruct’ (or usufruit) and can be used for residential property and investments. It can, however, cause complications if the property or asset is sold during the lifetime of the usufructuary, or if the donor decides to move back to the UK whilst keeping the usufruct in the property in France. It therefore requires care and specialist advice.

- Under French law, one’s marriage contract (régime matrimonial) is important in determining how assets will be distributed on death. It’s relatively easy to change your marriage regime if your current one isn’t appropriate for your situation. Often the ‘communauté universelle’ regime is chosen to provide better protection for the surviving spouse, but this won’t be the right choice for everyone.

- ‘Assurance-vie’ is a type of investment account that is outside of the scope of the normal succession rules and taxes, meaning the entire value can be left according to one’s wishes. It is potentially advantageous for all ages, but carries additional benefits for those who invest before the age of 70 – notably a tax-free succession allowance of €152,500 for each beneficiary. For these reasons and others, it is a powerful planning tool for those concerned about succession.

Succession planning is a highly personal issue and should be specific to your family situation and wishes. You need personalised advice and solutions.

Contact

Find out how to contact Blevins Franks here.

The tax rates, scope and reliefs may change. Any statements concerning taxation are based upon our understanding of current taxation laws and practices which are subject to change. Tax information has been summarised; an individual should take personalised advice. |